You moved back to India during the financial year. You earned a salary abroad for part of the year. You may now have an Indian salary, foreign tax records, and confusion about what to check before filing.

Returning to India brings reverse culture shock—especially when it comes to your taxes. The year you transition back is uniquely complicated because your income spans borders, tax jurisdictions, and different sets of rules.

If you simply hand over your Indian Form 130 (earlier form 16) to a CA or try to file a quick return online without addressing your foreign income, you are walking into a compliance trap. Failing to consolidate your global financial footprint correctly can lead to double taxation, defective returns, or lost tax credits.

This guide is built specifically for salaried professionals who relocated back to India this year. We will walk you through exactly how to map your income, gather the right documents, and choose the correct filing path.

30-Second Quick Answer Box

If you returned to India this year, first check these 4 things before you file:

Your residential status for the year

This dictates whether India taxes your global income or just your Indian income. Count your exact physical days in India.

Which income was earned before and after your return?

Grouping your income by when and where it was earned is crucial for avoiding double taxation.

Which foreign tax and salary documents you have?

You need specific proofs (like final payslips and foreign tax statements) to claim credit for taxes already paid abroad.

Whether your return needs extra schedules?

If you own foreign bank accounts, RSUs, or foreign income, you are legally barred from using the simple ITR-1 form.

Start here: know your situation before checking taxes

Step 1: First understand your return-year situation

Before jumping into tax forms, you need to establish the baseline facts of your transition year.

When did you return to India?

Your exact date of arrival dictates your physical presence in India during the financial year (April 1 to March 31). This number is the foundation of your “Residential Status.”

Under the law, if you spend 182 days or more in India, you are generally a Resident. However, depending on your income level and past stays, even 60 or 120 days can trigger resident status. Guessing this date can entirely change your tax liabilities.

Did you earn a salary only abroad, only in India, or both?

If you worked in Dubai until August and joined an Indian company in September, you have a split-income year. Your foreign salary might not be taxable in India if you qualify as a Non-Resident or a “Resident but Not Ordinarily Resident” (RNOR) for the year.

Conversely, if you continued working remotely for your foreign employer after moving back, that salary is deemed to accrue in India because the services were rendered on Indian soil.

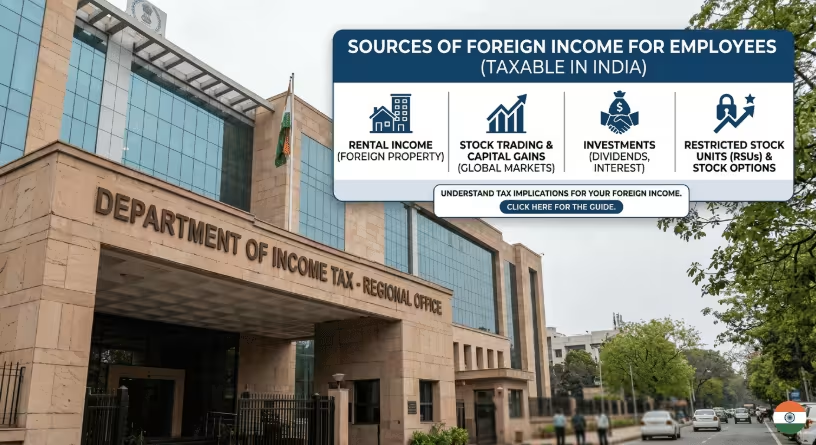

Are you only salaried, or salaried + side income?

Are you simply bringing home a paycheck, or did you also exercise foreign company stock options (RSUs), earn rental income abroad, or do freelance consulting? Keeping the scope clear helps you identify if you need a standard salaried return or a more complex business/capital gains filing.

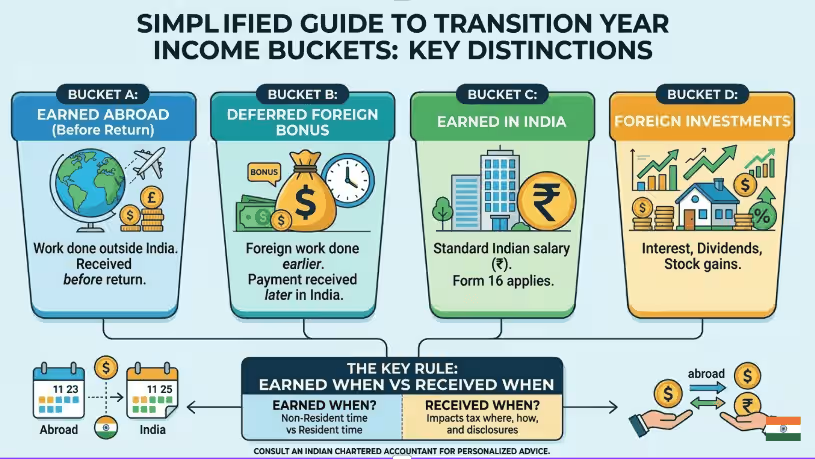

Map your income into simple buckets

Step 2: Split your income into buckets before you file

The biggest mistake returnees make is looking at their bank account deposits instead of how the income was earned. Salary timing and source often create confusion. Under the law, what matters is where the service was rendered and when it accrued, not just when it hit your bank.

To get clarity, map your transition year into these buckets:

Bucket A: Salary earned abroad before returning. (e.g., Your final months working in the US/UK/UAE).

Bucket B: Salary/bonus paid later but related to your foreign employment period. (e.g., An annual bonus paid in December for work you finished abroad in June).

Bucket C: Salary earned in India after joining here. (e.g., Your standard Indian employment covered by Form 130).

Bucket D: Foreign interest/dividend/RSUs. (e.g., Dividends from foreign stocks or interest from an overseas savings account).

Why this matters: You must separate “earned when” from “received when.” For example, if Bucket A was earned while you were a non-resident, it generally isn’t taxed in India. But if Bucket B hits your Indian bank account directly after you become a resident, it might trigger different disclosure requirements.

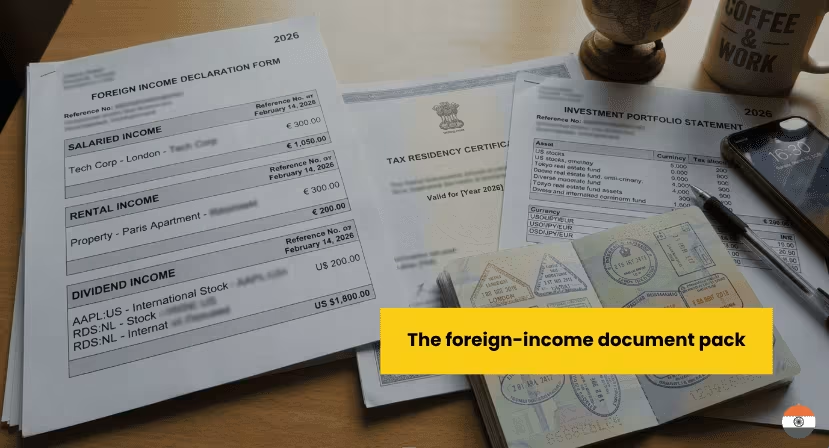

The foreign-income document pack

Step 3: Collect this document pack before you start filing

Do not start filing your ITR without these records. If you need to claim relief on taxes you paid abroad, the tax department requires specific, verified evidence.

- Identity and travel proof

- Passport: To count your physical days in India (including arrival/departure stamps).

- Visa / travel history: To prove your residency status across the last 4 to 10 years, which is required to claim the beneficial RNOR status.

- Boarding passes / tickets: As backup proof of your exact return date.

- Foreign employment and foreign tax proof

- Foreign salary slips & annual pay summary: For the months worked overseas.

- Foreign tax return / tax statement: Documents like a US W-2/1040 or UK P45.

- Tax deduction proof: To claim a Foreign Tax Credit (FTC) in India, you legally need a certificate from the foreign tax authority, a statement from your employer, or a self-signed statement backed by an online bank payment counterfoil.

- India-side filing proof

- Form 130 (Earlier Form 16): From your Indian employer (if applicable).

- Annual Information Statement (AIS): The tax department’s master record (Form No. 168) of your Indian financial footprints.

- Indian bank statements & investment records: For local deductions (Section 80C, etc.).

Check Out: “Foreign Income Documents salaried employees should collect before filing their first ITR"What to check before you assume your filing path

Step 4: Check these filing questions before choosing your return path

Before logging into the tax portal, run your profile through these four checks.

What is your residential status for this year?

Are you a Non-Resident (NR), Resident but Not Ordinarily Resident (RNOR), or a full Resident? If you were a non-resident in 9 out of the 10 preceding years, you usually qualify as RNOR upon return. This is a “honeymoon” status where your foreign income (like Bucket A and D) generally remains exempt from Indian taxes, unless it is derived from a business controlled in India.

Do you need to think about foreign tax credit?

If your status makes your foreign salary taxable in India, did you already pay tax on it abroad? India has Double Taxation Avoidance Agreements (DTAA) with many countries. To ensure you aren’t taxed twice on the same income, you must claim a Foreign Tax Credit by filing Form No. 44 before or alongside your return.

Do foreign assets/income disclosures need your attention?

If you qualify as an ordinary Resident, you are legally required to disclose all foreign assets—including bank accounts, equity shares (RSUs), and properties—in your tax return, even if they generate zero income.

Is your case still a simple salaried filing?

If you retain a foreign bank account, hold foreign assets, or need to claim DTAA relief, you are strictly prohibited from using the simple ITR-1 (SAHAJ) or ITR-4 forms. You will automatically be bumped up to ITR-2 (or ITR-3 if you have business/freelance income). Using ITR-1 when you have foreign assets will render your return defective.

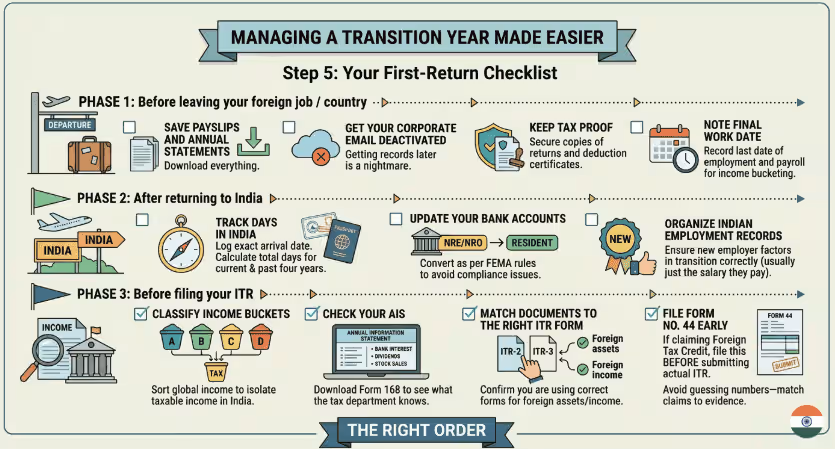

The actual checklist in chronological order

Step 5: Your first-return checklist in the right order

Managing a transition year is much easier if you break it into three phases.

- Before leaving your foreign job / country

- Save payslips and annual statements: Download everything. Once your corporate email is deactivated, getting these records is a nightmare.

- Keep tax proof: Secure copies of your foreign tax returns and official tax deduction certificates.

- Note final work date: Record your last date of employment and your last payroll date for clean income bucketing.

- After returning to India

- Track days in India: Log your exact arrival date. Check your passport to calculate your total days in India for the current year and the preceding four years.

- Update your bank accounts: Convert your NRE/NRO accounts to normal resident savings accounts as per FEMA rules to avoid compliance issues.

- Organize Indian employment records: Ensure your new Indian employer factors in your transition correctly (though they will usually only deduct tax on the salary they pay you).

- Before filing your ITR

- Classify income buckets: Sort your global income into the A/B/C/D buckets to isolate what is actually taxable in India.

- Check your AIS: Download your Annual Information Statement (Form 168) to see what the Indian tax department already knows about your local bank interest, dividends, and stock sales.

- Match documents to the right ITR form: Confirm you are using ITR-2 or ITR-3 if you have foreign assets or foreign income.

- File Form No. 44 early: If claiming Foreign Tax Credit, file this form before submitting your actual ITR. Avoid guessing numbers where records are incomplete—match your claims to your documentary evidence.

Common mistakes returning salaried employees make

Step 6: 7 mistakes to avoid in your first return year

Even with the best intentions, the transition year trips up many returning professionals. Here are the seven most common traps to avoid:

Mixing up your return date and salary period

The law doesn’t just look at when you got paid; it looks at your physical presence in India. Your exact arrival date determines whether you are a Resident, Non-Resident (NR), or Resident but Not Ordinarily Resident (RNOR). Guessing this date can drastically alter your tax liability.

Not saving foreign payslips before access is lost

Once you leave your overseas job, you usually lose access to the company portal. If you need to claim a Foreign Tax Credit (FTC) in India to avoid double taxation, you are legally required to provide a certificate of tax deduction or a self-signed statement backed by proof of payment. Without payslips or a foreign tax return, you cannot validate this claim.

Assuming all foreign income works the same way

A salary earned while you were a non-resident is treated differently than a dividend paid into your foreign bank account after you become an Indian resident. The law taxes income based on whether it is received in India, accrued in India, or if you are a full resident, your global income.

Filing before checking if extra schedules or proofs matter

If you are claiming credit for taxes paid abroad, you must file Form No. 44 before or on the date you furnish your updated return. Filing your main ITR without submitting this form first can cause you to lose your tax credit entirely.

Forgetting late-paid foreign bonuses or dues

If your foreign employer pays out your annual bonus months after you have relocated and become an Indian resident, that money might be taxable in India depending on your residency status and Double Taxation Avoidance Agreements (DTAA).

Ignoring side income because “mainly I’m salaried”:

Did you get a few dollars in interest from your overseas savings account? Do you hold foreign stocks or RSUs? Having assets or signing authority in an account outside India legally bars you from using the simple ITR-1 or ITR-4 forms. You must declare these, or your return will be considered defective.

Waiting too late to reconstruct documents

The Indian tax department tracks foreign remittances and specified financial transactions through your Annual Information Statement (AIS). If you wait until the filing deadline to gather your documents, you won’t have time to reconcile discrepancies between your records and the government’s data.

Conclusion

Returning to India as a salaried professional in 2026 demands more than just a simple salary disclosure; it requires a proactive approach to global financial consolidation. The “Foreign-income tax checklist for salaried employees 2026” emphasizes that your transition year filing is a high-compliance event where the residential status “day-count” acts as the master lever for your tax liability. With the 2026 tax landscape introducing stricter nudges for Schedule FA (Foreign Assets) and the mandatory electronic filing of Form 67—or its potential successor, Form 44—before your ITR, accuracy is no longer optional.

Neglecting to separate your pre-return foreign salary (Bucket A) from late-paid bonuses or dividends (Bucket B/D) can trigger unintended double taxation or severe penalties under the Black Money Act. By strictly following this checklist, matching your income to the correct ITR-2 or ITR-3 form, and ensuring your NRE/NRO accounts are redesignated according to FEMA, you can secure your “honeymoon” RNOR status and protect your hard-earned global savings from compliance traps.

Frequently Asked Questions (FAQs)

Do I have to report foreign salary if I return to India mid-year?

It depends entirely on your residential status. If your stay in India qualifies you as a “Non-Resident” (NR) or “Resident but Not Ordinarily Resident” (RNOR) for that specific tax year, your foreign salary is generally not taxable in India unless it was received directly in India or derived from an Indian business. If you qualify as a full Resident, your global income is taxable in India.

What documents should I keep from my foreign employer?

Do not leave the country without your final payslips, an annual pay summary, your official foreign tax return (if applicable), and a certificate of tax deduction. If you need to claim credit in India for taxes paid abroad, the tax department requires verifiable proof.

What if I received foreign salary after returning to India?

If the salary was for services rendered abroad but paid out later, its taxability depends on whether it was directly remitted to an Indian bank account and your residency status. Income received or deemed to be received in India is generally taxable across all residency statuses.

Can a salaried returning employee still have a complex return?

Absolutely. If you hold Employee Stock Ownership Plans (ESOPs), Restricted Stock Units (RSUs), or even just a basic savings account in your former country of residence, you are barred from filing the simple ITR-1 form and must file a more complex return like ITR-2.

Leave a Reply