Foreign income documents for salaried employees should collect before filing their first ITR. If you returned to India during the financial year, worked abroad for part of the year, and now hold a mix of foreign salary records and Indian salary records, this guide is for you.

This checklist is designed to help you keep the right documents organised before tax filing so you do not face compliance traps or double taxation later.

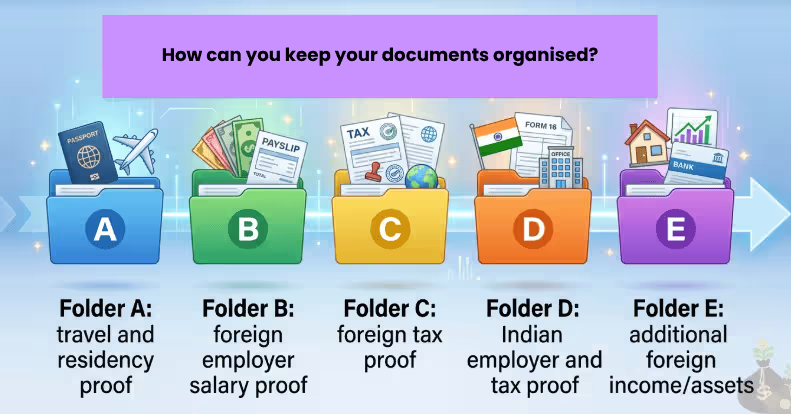

Quick answer: the 5 document groups you should maintain

1. Identity and travel documents

(Passports, visas, and entry/exit stamps to prove your residency status).

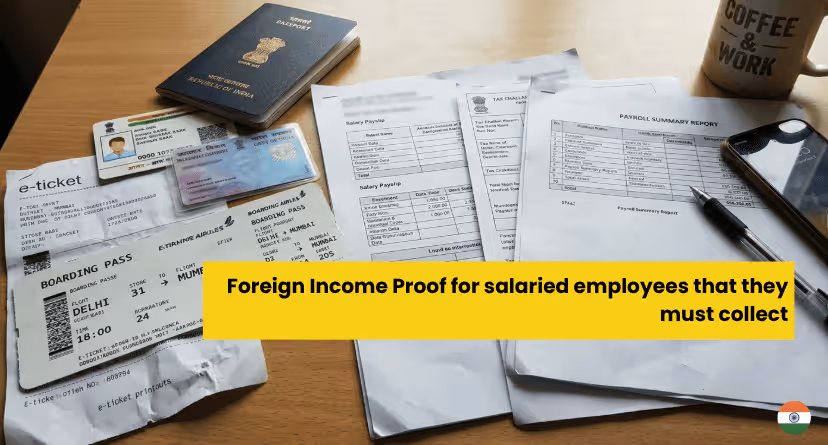

2. Foreign employment and salary proof

(Foreign payslips and separation records for your time abroad).

3. Foreign tax proof

(Tax returns, withholding statements, and challans to claim tax credits in India).

4. India salary and tax documents

(Form 16/Form 130, Indian payslips, and deduction declarations).

5. Supporting records for foreign income/assets, if any

(Statements for overseas bank accounts, RSUs, or properties).

Identity and return-date documents

Everything in your transition-year tax return depends on your physical movement. India taxes individuals based on their residential status, which is strictly calculated using your physical days present in the country during the tax year and preceding years.

- Passport and visa records

- Your passport and visa are your primary identity and travel proofs. Competitors often list these as core documents, but in a return-year case, they are specifically needed to prove your historical travel timeline to establish if you qualify for beneficial tax statuses like “Resident but Not Ordinarily Resident” (RNOR).

- Entry and exit stamps / travel history

- You become a resident if you are in India for 182 days or more in the tax year, or 60 days (120 days for Indian citizens with Indian income over ₹15 lakhs) if you were in India for 365 days in the previous four years. You must rely on the exact entry and exit stamps in your passport, not estimates, because miscounting by a single day can alter your entire tax liability.

- Return date proof and relocation records

- Keep your boarding passes and flight tickets. If there is ever a dispute or scrutiny regarding the exact date you resumed your physical presence in India, these relocation records serve as the ultimate tie-breaker.

Check Out: “Returned to India mid-year? A first-return foreign-income tax Guide for salaried employees 2026"Foreign employment and salary documents

This is the biggest pain point for salaried employees. Salary is deemed to accrue where the services are rendered. You must build a clean salary file for the period worked abroad to separate your non-taxable foreign income from your taxable Indian income.

- Foreign employment contract / offer / separation records

- These documents prove the exact start and end dates of your overseas employment. They help establish that the income earned during this specific window was for services rendered outside India.

- Foreign payslips for the period worked abroad

- Always download your foreign salary slips before losing access to your employer’s portal. These are the most heavily requested documents because they provide a month-by-month breakdown of what you earned while you were a non-resident versus what you earned after returning.

- Annual compensation or payroll summary from the foreign employer

- An annual summary (like a W-2 or P45) aggregates your overseas earnings and taxes. It is essential for reconciling your total foreign income before you file your Indian return, ensuring no discrepancies exist between your declared income and your employer’s records.

- Bonus, deferred payout, or final settlement records

- Under the law, salary includes any arrears or advances paid to you, even if paid by a former employer. If you receive a bonus or final settlement after returning to India that relates to your time abroad, you will need these records to determine if that payout is taxable in India based on your current residency status.

Foreign tax proof documents

If your foreign salary becomes taxable in India (for example, if you qualify as a full Resident for the year), you can usually claim a Foreign Tax Credit (FTC) to avoid paying tax twice on the same income.

- Foreign tax return copy, if filed

- To claim credit for taxes paid in a country outside India, you are required to file a statement of income from that country and the foreign tax deducted on it using Form No. 44. Having a copy of your filed foreign tax return makes computing these numbers straightforward and verifiable.

- Foreign tax withheld statement / employer tax summary

- You must prove the tax was actually paid. The rules mandate that you provide a certificate or statement specifying the nature of the income and the tax deducted from either the foreign tax authority or the person responsible for the deduction (your employer).

- Tax payment challans or payment confirmations, if applicable

- If an official tax certificate is not available, you can provide a self-signed statement, but it must be accompanied by an acknowledgment of online payment, a bank counterfoil, or a challan proving you paid the tax.

- Tax Residency Certificate or similar residency proof, where relevant

- If you are claiming relief under a Double Taxation Avoidance Agreement (DTAA), you must obtain a certificate of your being a resident from the Government of that foreign country or specified territory. This proves to the Indian tax department that you were indeed a tax resident of the other country during the period in question.

India salary and tax documents after return

Once you start working in India, you are back in the standard domestic tax system. These documents ground your file in your “returned this year” reality.

- Indian offer letter / joining proof

- This establishes the date you commenced providing services on Indian soil, which is the exact point your salary begins accruing in India and becomes taxable regardless of your residency status.

- Indian salary slips

- Keep these to track your monthly gross receipts, local allowances, and local tax deductions.

- Form 130 (Earlier Form 60)

- Under the new rules, the certificate for tax deducted at source on your salary by your employer is issued in Form No. 130 (traditionally known as Form 16). This is the master document for your Indian salary filing.

- Form 12BB and deduction proofs submitted to employer

- To claim exemptions for things like House Rent Allowance or Leave Travel Concession through your payroll, you must furnish evidence of your claims to your employer. Under the latest rules, this is done using Form No. 124. Keep a copy of this form and all underlying rent receipts or travel tickets.

India-side tax records you should keep with your file

These are the supporting pillars of your tax file.

- PAN and Aadhaar

- Your Permanent Account Number (PAN) and Aadhaar are mandatory for filing. Ensure they are linked and updated with your current Indian residential address.

- AIS / Form 26AS / TDS records

- The tax department tracks your financial footprints. They will upload an Annual Information Statement (Form No. 168) to your registered online account containing details of your TDS, specified financial transactions, and tax payments. Always cross-check this against your own records before filing.

- Indian bank statements

- Keep statements for all your Indian savings accounts, NRE/NRO accounts, and current accounts. They are necessary for calculating your taxable interest income.

- Deduction and investment proofs, where relevant

- Keep receipts for life insurance premiums, PPF contributions, ELSS mutual funds, or medical insurance to claim your Chapter VIII local deductions.

Foreign income or asset support documents, if applicable

Note: If you hold any of the following, your tax return ceases to be a simple salaried filing.

- Foreign bank account statements

- Interest or dividend statements

- Foreign brokerage / stock holding statements

- Property income records, if any

If you own assets outside India (like a bank account, RSUs, or property), have a financial interest in an entity outside India, or possess signing authority in any foreign account, you are legally barred from using the simple Form SAHAJ (ITR-1) or Form SUGAM (ITR-4). You must use a more comprehensive form like ITR-2 or ITR-3 and thoroughly disclose these holdings using your foreign statements.

Common document mistakes salaried employees make

Even the most meticulous professionals make documentation errors during their transition year back to India. Because international tax compliance requires very specific proofs, missing even one document can cause major headaches. Here are the most critical mistakes to avoid:

- Losing access to your foreign payroll portal after resignation: Once you hand over your corporate laptop, you usually lose access to your digital HR portal. If you need to claim a Foreign Tax Credit (FTC) in India, you are legally required to furnish a certificate or statement specifying the nature of income and tax deducted. Always download your complete file before your last working day.

- Only saving monthly payslips but not the annual summary: While monthly payslips are helpful for your own tracking, your annual pay summary (like a US W-2 or UK P45) is what actually aggregates your total foreign income and final tax liabilities. Without this summary, it is incredibly difficult to correctly file Form No. 44, which is mandatory for claiming credit on foreign taxes paid.

- Not keeping return-date proof: Your entire Indian tax liability hinges on your “Residential Status,” which is calculated by the exact number of days you are physically present in India (such as the 182-day or 60-day thresholds). Do not throw away your old boarding passes or flight tickets; they are your ultimate tie-breaker if the tax department questions your arrival date.

- Not saving foreign tax proof before leaving the country: To get relief from double taxation under Double Taxation Avoidance Agreements (Section 159) or from countries without an agreement (Section 160), you must prove you actually paid the tax abroad. If you don’t have an official certificate, you will need to rely on self-signed statements backed by online bank payment counterfoils or challans. Secure these before you close your overseas bank accounts.

- Mixing foreign and Indian salary records into one folder: Under the law, the taxability of your income strictly depends on whether it accrued in India or outside India. Mixing these records leads to confusion, making it easy to accidentally pay Indian taxes on foreign income that should be completely exempt. Keep your “earned abroad” and “earned in India” document buckets strictly separated.

- Assuming Form 130 alone is enough: Your Indian employer will provide a certificate for tax deducted at source for your Indian salary—now officially issued under the new rules as Form No. 130 (or Form No. 123 if your salary is over ₹1.5 lakhs). However, this document only covers the salary earned in India. If you hold foreign bank accounts, RSUs, or foreign income, you are legally required to file a comprehensive return disclosing those global assets and cannot rely on your Indian salary certificate alone

Leave a Reply