Handle a 142(1) Notice under Income Tax Act, 1961 with care either doing it yourself or with assistance from an expert, that is CA. Navigate with following things to make a sound decision for yourself that saves you from cost.

Quick Answer

Cases many salaried professionals can handle a 142(1) Notice themselves

For standard salaried employees, many automated inquiry notices are straightforward and do not require expensive professional fees. You can safely manage the response via the designated e-filing portal yourself if:

- You simply forgot to file: The notice asks you to furnish a return of your income because you missed the deadline, and your income consists purely of standard Indian salary and basic savings interest.

- A specific deduction proof is missing: The Assessment Unit is asking you to produce specific accounts or documents, such as a rent agreement to justify your House Rent Allowance (HRA) or an investment receipt for a Section 80C claim.

- Clarifying a specific bank entry: The notice asks you to explain the source of a specific high-value deposit (like a gift from a parent) that was flagged in your Annual Information Statement (Form No. 168). You can simply reply in writing and attach the relevant bank statement and a gift deed.

Discover More Related Post

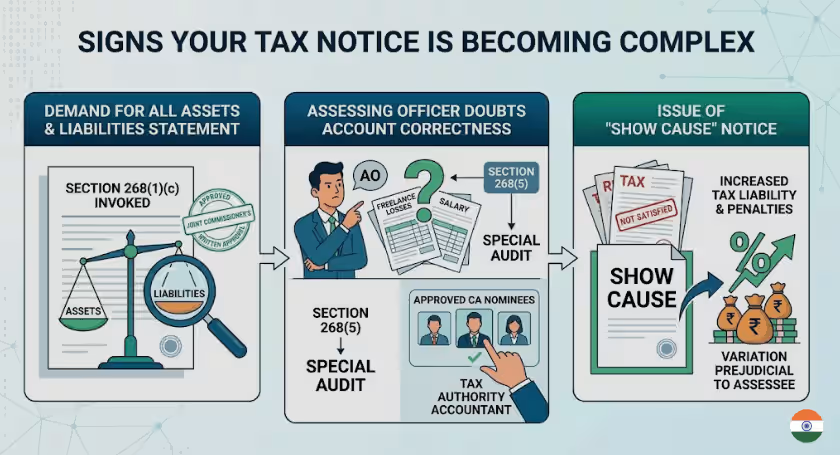

Signs your notice is becoming complex

While many notices are routine, certain legal triggers within a Section 268(1) notice indicate that the tax department is digging deeper. Watch out for these specific signs:

Demand for a “statement of all assets and liabilities”

If the notice invokes Section 268(1)(c) asking for a complete breakdown of your assets and liabilities (whether included in your accounts or not), it means the Assessing Officer has already escalated your case and obtained prior, written approval from a Joint Commissioner to thoroughly investigate your net worth.

When the AO expresses “doubts about the correctness of the accounts”

If the AO severely doubts the correctness of your financial claims (for example, you claim massive freelance business losses alongside your salary), they can invoke Section 268(5) to order a special audit. Here, you absolutely need a CA.

The AO will direct you to get your accounts audited by a nominated “accountant” (a practicing Chartered Accountant). This requires a strategic trail of answering because the CA’s audit report (Form No. 100) will directly influence whether the AO slaps you with a massive penalty for misreporting.

Who nominates them? You do not get to pick your own CA for this. To ensure strict neutrality, the tax authorities (specifically the Principal Chief Commissioner or Commissioner) will “nominate” an accountant from their own approved government panel to audit you.

Progression to a “Show Cause” Notice

If the Assessment Unit is not satisfied with the documents you provided, they will issue a show cause notice proposing a “variation prejudicial to the interest of the assessee” (i.e., they plan to increase your tax liability).

When CA help is strongly recommended

Do not attempt a DIY response if your notice involves any of the following high-risk areas:

- Foreign Assets and RSUs: If the inquiry involves unvested Restricted Stock Units (RSUs) from your global employer, foreign bank accounts, or Double Taxation Avoidance Agreement (DTAA) relief. Algorithms and faceless officers often heavily scrutinise international transactions, and you need a CA to correctly apply treaty rules.

- General Anti-Avoidance Rule (GAAR) references: If the notice mentions Section 274 or suspects your tax setup is an “impermissible avoidance arrangement” (e.g., routing consulting income through a shell entity). This is a highly strategic legal battle that can escalate to an elite Approving Panel headed by a High Court Judge.

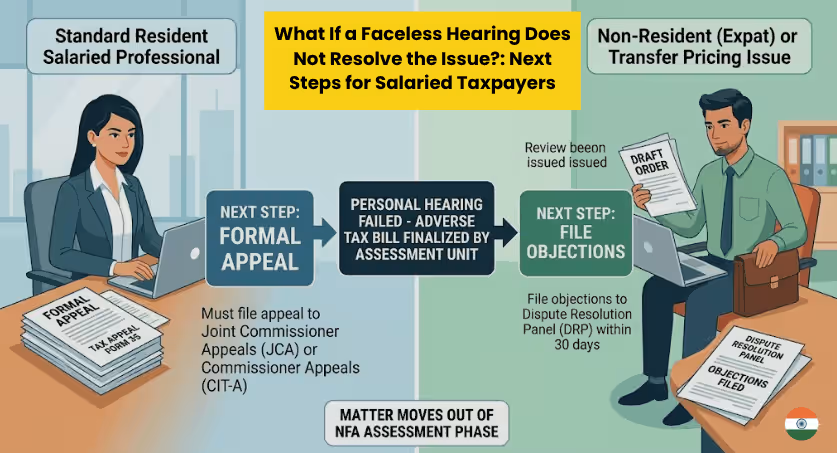

- Non-Resident Draft Orders: If your residential status is Non-Resident (NR) or Resident but Not Ordinarily Resident (RNOR), and the department issues a “Draft Order” under Section 275 proposing to increase your tax. You only have 30 days to file objections directly with the Dispute Resolution Panel (DRP).

- You need a Personal Hearing: If you need to defend yourself orally, you have the right to a personal hearing conducted exclusively via video conferencing or video telephony. A CA can represent you as an “authorised representative” under Section 515 during this critical video call.

Check Out: When Can You Request a Personal Hearing After an Income-Tax Notice 2026?What a CA actually helps with

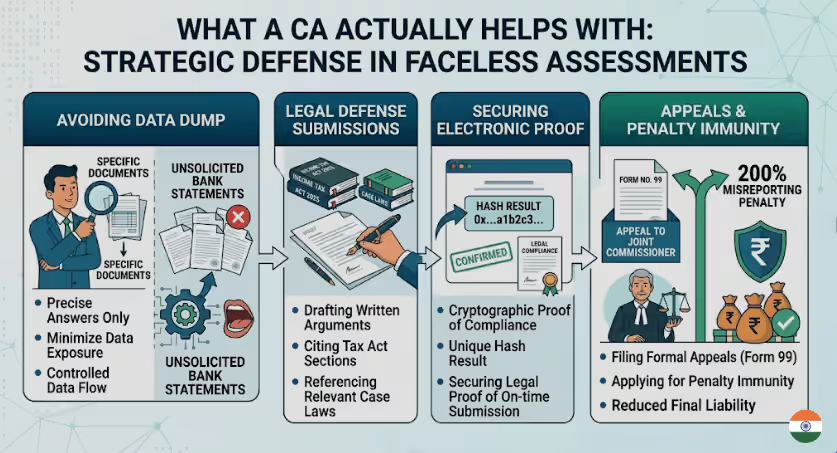

CA does far more than just upload PDFs to the tax portal. In a faceless assessment environment, they provide strategic defence:

- Avoiding the “Data Dump”: CAs know exactly how to answer the specific question asked without volunteering extra, unasked-for bank statements that give the automated examination tools more data to scrutinize.

- Drafting Legal Submissions: Because you cannot meet the officer, your entire defence relies on written submissions to the NFAC. A CA will draft your response citing specific sections of the Income-tax Act 2025 and relevant case laws.

- Securing Electronic Proof: A CA ensures that every response submitted to the NFAC receives an acknowledgement containing a unique “hash result”. This cryptographic footprint is your absolute legal proof that you complied with the notice on time.

- Appeals and Immunity: If the Assessment Unit finalizes an adverse tax bill, your CA will file a formal appeal (Form No. 99) before the Joint Commissioner (Appeals). Alternatively, they can help you apply for immunity from the 200% misreporting penalty if you choose to pay the tax demand.

What to prepare before speaking to a CA

To save time and ensure your CA can properly evaluate your Section 268(1) notice, gather these documents before your consultation:

- The exact Notice and the Hash Result: Download the full PDF of the notice from your registered e-filing account on the designated portal.

- Your Annual Information Statement (AIS): Download Form No. 168 from the portal so the CA can see the exact high-value transactions or mismatches the tax department is looking at.

- All Salary Certificates: Gather every Form No. 130 (the new equivalent of Form 16) issued by your employers for the relevant tax year.

- Travel History: If the inquiry touches upon your residential status or foreign income, prepare a precise list of your entry and exit dates from India based on your passport stamps.

Conclusion

Not every case requires the assistance of CA. In cases like where you have forgotten to file your return or there is a basic clarification needed or certain proofs are required can handled by salaried professionals themselves just by following right steps.

However, the assistance of an expert becomes Paramount when you are involved in complex transactions, then, CA is highly recommended. Only an expert can navigate you strategically in the Faceless Assessment process on your behalf. But before that you have to accumulate all the necessary documents for consultation. These articles would help the salaried professional to handle the Tax Notices situation in prompt.

Leave a Reply