Draft Income-Tax Rules 2026: may change payroll for salaried employees in FY 2026–27. See key updates, what affects take-home pay and TDS, and a simple checklist for you and HR. When HR/payroll changes happen for FY 2026–27, what is the immediate action plan for a salaried employee? What is actually affecting their ‘wallet’?

Here’s your essential survival guide to Draft Income Tax Rules, 2026.

Think of it not just as a “tax update” but as a major renovation of your salary slip in the last decades. Released on February 9th 2026, these draft rules acknowledge that living costs in 2026 are very different from the 1990s. While some perks just saw a massive upgrade, others (like that company car) might cost you more now. This guide decodes those significant administrative changes (mandatory forms), discovers new limits and hidden valuation tweaks that might affect your take-home pay.

Here’s the checklist of key payroll changes that you need to know to protect your take-home pay:

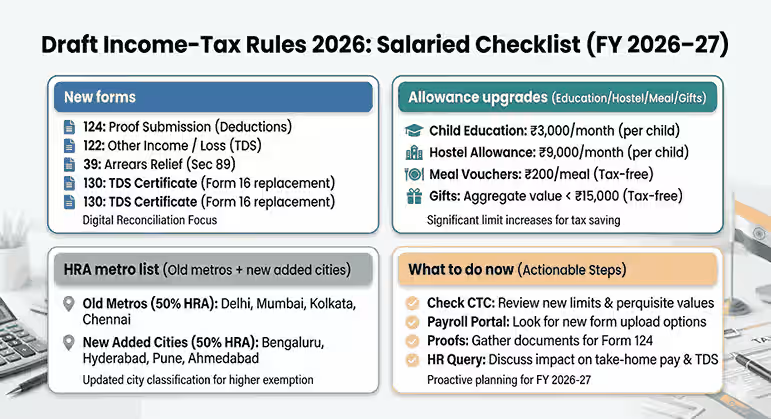

Paperwork Alert: The updated forms that you must know

Brief: The draft rules mandate specific forms for communicating with your employer for tax deductions. These forms are designed in a way that facilitates digital reconciliation therefore these forms are no longer any casual or declarative form like before.

| Old forms (Rules 1962) | New form (Draft rules 2026) | Name of the form |

| Form 12BB | Form 124 | “The proof submission form” |

| Form 10F | Form 122 | “The other income form” |

| Form 10CCAC | Form 39 | “The arrears relief form” |

| Form 16 | Form 130 | “TDS Certificate” |

| Form 12BA | Form 123 | “Perquisite Statement” |

Mandatory Tax Forms You Need to Track Today:

- Form 124: The mandatory form to furnish evidence of your claims or expenditure.

Action: Under Rule 205, an employee must submit Form No. 124 to their employer to claim deductions like HRA, LTA, or interest on home loans.

- Form 122: This form used to report income other than your salary (or losses like home loan interest) to your employer.

Action: Under Rule 204, If you want your employer to adjust your TDS accurately so you don’t have to pay extra tax later, Submit this form declaring your side income or house properly loss.

- Form 39: If you have received salary arrears, advance salary, or family pension in arrears, you are eligible for tax relief under section 157(1) [formerly section 89].

Action: Under Rule 73, Do not wait for your ITR refund. Submit this form to your employer immediately upon receiving arrears. This authorises them to calculate the relief and reduce the tax deducted from your paycheck,

- Form 130: This is the main TDS Certificate certifying that tax was deducted from your salary and deposited with the government.

Action: Ensure you receive Form 130 from your employer by 15th June of the financial year immediately following the tax year (e.g., for tax year 2026-27, receive by June 15, 2027).

- Form 123: A detailed Statement of Perquisites (benefits like rent-free accommodation, cars, ESOPs) provided by the employer.

Action: Open your Form 130 (the main TDS certificate) and look at the “Total Value of Perquisites” section. The aggregate total at the bottom of Form 123 must perfectly match the single line-item figure reported in Form 130.

As per Rule 204, Your employer will now issue:

• Form No. 123: If your salary is more than Rs. 1,50,000 in the tax year.

•Form No. 130: If your salary is Rs. 1,50,000 or less

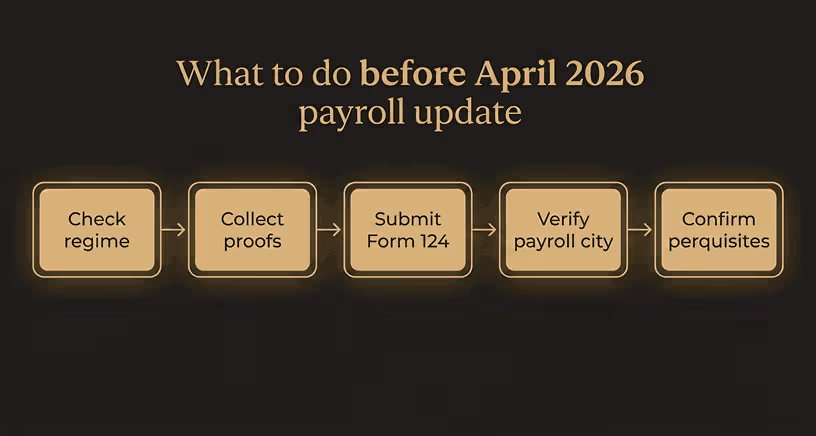

What to check: Your company’s payroll portal, confirm these specific forms are available for upload.

“For a complete breakdown of this year’s changes, browse our latest tax updates.”

Salary structuring: Maximize your “wallet”

Review your cost to your company breakdown against these new limits specified in Rule 280 to ensure you aren’t missing out on a tax free income.

| Allowance Type | Before (Draft Rules 2026) | After (Draft Rules 2026) |

| Child Education | ₹100 per month per child | ₹3,000 per month per child |

| Hostel Allowance | ₹300 per month per child | ₹9,000 per month per child |

| Travel (For Disabled) | ₹3,200 per month | ₹8,000 (Non-Metro) / ₹15,000 (Metro) |

| Travel (Transport Staff) | ₹10,000 per month cap | ₹25,000 per month (cap) |

Check Out: PAN Quoting Rules 2026: Compliance Guide for Salaried EmployeesFollowing are upgraded allowances that actually save you money:

- Child Education allowance

Action: Ensure your employer allocates Rs. 3000/- per month per child (up to 2 children). This is a massive jump from the historical limit.

- Hostel Allowance

Action: If your children live in a hostel, ask for Rs. 9,000 per month per child. This offers a potential tax exemption of Rs. 2.16 Lakhs annually for two children

- Travel allowances

Action: If you are working in the transport sector like railways, airlines, or shipping, then draft rules keep the 70% limit but more than double the monthly cap to Rs.25,000. Ensure this change reflects in your payslip.

What to check: Your “Annexure to Appointment Letter” or current CTC breakdown to see if you are still stuck on the old, lower limits.

HRA Strategy: The “New Metro” List

If you rent in a major tech hub, your exemption calculation has officially changed. Rule 279 explicitly lists Bengaluru, Hyderabad, Pune, and Ahmedabad (alongside Delhi, Mumbai, Kolkata, Chennai) as cities where you are entitled to a 50% of salary exemption for HRA.

Action: If you live in one of these cities, ensure your payroll system is calculating your exemption at 50% (not the standard 40% for non-metros)

What to check: If it still shows 40%, contact your HR or Finance team to update your city classification based on the new Rule 279 guidelines.

Check Out: Audit Before Claiming HRA: The 7-Point Compliance Checklist for 2026 Tax RulesPerquisite Audits: Check your taxable value

Meal & Gift-Voucher

These are the easiest ways to increase your take-home pay.

- Meal Vouchers: Food/ non – alcoholic beverages provided during working hours were increased from Rs.50 to Rs. 200 per meal.

- Gifts: Gifts, vouchers, or tokens are tax-free if the aggregate value during the tax year is less than Rs.15,000.

Action: Ensure your daily meal coupon is optimized to Rs.200 per meal to maximize tax free benefit. This shift alone can make Rs.1,05,600 per year of your salary tax-free.

What to check: Check if your company still offers the old Rs.50/meal limit.

Motor Car

Through these rules, the taxable value of company- provided cars has nearly tripled in 2026-27. Therefore, employees might see a sudden drop in their April 2026 take-home pay because the employer must deduct more TDS to cover the higher perquisite value.

Scenario A: Employer pays for Fuel & Maintenance

| Engine Capacity | Old Rules (1962) | Draft Rules (2026) |

| Up to 1.6 Litres | ₹1,800 / month | ₹5,000 / month |

| Above 1.6 Litres | ₹2,400 / month | ₹7,000 / month |

| Chauffeur (Driver) | + ₹900 / month | + ₹3,000 / month |

Scenario B: Employee pays for Fuel & Maintenance

| Engine Capacity | Old Rules (1962) | Draft Rules (2026) |

| Up to 1.6 Litres | ₹600 / month | ₹2,000 / month |

| Above 1.6 Litres | ₹900 / month | ₹3,000 / month |

| Chauffeur (Driver) | + ₹900 / month | + ₹3,000 / month |

Action: If your car is small but HR is taxing you at the “Large Car” rate, correct them using Rule 15 (Table II)

What to check: Review your “Car Lease” or “Conveyance” component in your CTC and ask your payroll team for a tax impact simulation before the new FY starts.

Leave travel concession under Draft Income tax Rules, 2026 (LTC Planning)

Brief: If you are planning a trip this year with your family within India, your tickets might prove to be a powerful tool to shrink your taxable income under the new draft income tax framework 2026.

| Travel Mode | Old Rules (1962) | Draft Rules (2026) |

| Air Travel | Capped at economy class fare of the national carrier by the shortest route. | Limited to the fare admissible for the class of travel to which the employee is entitled via the shortest route. |

| Rail Travel | Exemption limited to AC First Class rail fare by the shortest route. | No change |

| Road Travel (No Public Transport) | Linked to the amount that would be incurred if the journey were performed by AC First Class rail. | Explicitly codified at a fixed rate of ₹30 per kilometre for the distance of the shortest route. |

| Road Travel (Public Transport Exists) | Limited to first class or deluxe class fare on such transport. | No change |

Action:

- Ensure your travel occurs within the current four-year block (2022–2025). One unutilized journey can be carried forward to the first calendar year of the next block (2026).

- You must be on official leave from work to qualify; travel during weekends or public holidays without formal leave does not count.

- Preserve all original travel documents, including tickets, boarding passes, and receipts.

- Use Form No. 124 (Rule 205) to submit evidence to your employer for accurate TDS estimation.

What to check:

- Ensure family members included in the claim (spouse, children, dependent parents/siblings) meet the dependency criteria.

- Confirm your claim only includes up to two surviving children, unless the children were born before October 1, 1998, or in cases of multiple births after the first child.

- Confirm you are opting for the Old Tax Regime, as LTC exemptions are not available under the New Tax Regime.

- Verify that the entire journey is within India, as international trips are completely ineligible.

Conclusion

As we are transitioning into FY 2026-27, Draft Income-Tax rules 2026 emerged as a double edge sword of a working salaried person. One hand, the renovation of stagnant limits for education, hostel, meal voucher offers a significant relaxation, But on the other hand, sharp rise in motor car valuations and shift to more rigid, digital-ready forms like Form 124, 122, and 39 which means that ‘casual declaration’ is a thing of past.

The key takeaway for every salaried employee is pro-activity. By auditing your CTC now, verifying your city’s metro status for HRA, and ensuring your payroll department is ready for the new perquisite math, you aren’t just filing taxes—you are actively protecting your monthly take-home pay.

Don’t wait for your April payslip to discover these changes. Use this checklist to start the conversation with your HR and Finance teams today.

Here’s the complete list to easily navigate from old income tax form, 1962 to new tax form, 2026:

Comparing old and new tax forms under draft income tax rules, 2026

Frequently Asked Questions [FAQs]

Q1: Are gift vouchers from my employer taxable?

They are tax-free only if the aggregate value is Rs. 15,000 or less during the tax year. If the value exceeds this, the entire amount may be treated as a taxable perquisite.

Q2: Do I need to submit any specific form to my employer to claim HRA or Home Loan interest?

A: Yes. Under Rule 205, you must furnish Form No. 124 to your employer. This form requires details like the name, address, and PAN of your landlord (for HRA) or lender (for home loans).

Q3: How is the tax calculated on my company car under the 2026 rules?

A: It is based on engine size. Under Rule 15, if the car is owned by the employer and used for both personal and official work:

• Engine ≤ 1.6 Litres: Taxable perk is ₹5,000/month.

• Engine > 1.6 Litres: Taxable perk is ₹7,000/month.

• Driver provided? Add: ₹3,000/month

Q4: I live in Bengaluru. Can I now claim 50% HRA exemption like in Delhi?

A: Yes. The Draft Rules 2026 explicitly list Bengaluru, Hyderabad, Pune, and Ahmedabad alongside the original four metros (Delhi, Mumbai, Kolkata, Chennai) for the 50% salary exemption limit on HRA.

Q5: I play online rummy. Do I only pay tax when I withdraw money?

A: No. Under Rule 135, your “Net Winnings” include the closing balance in your user account at the end of the year. The formula is:

(Withdrawals + Closing Balance) – (Deposits + Opening Balance).

You are taxed on money sitting in the app wallet, not just what hits your bank.

Leave a Reply