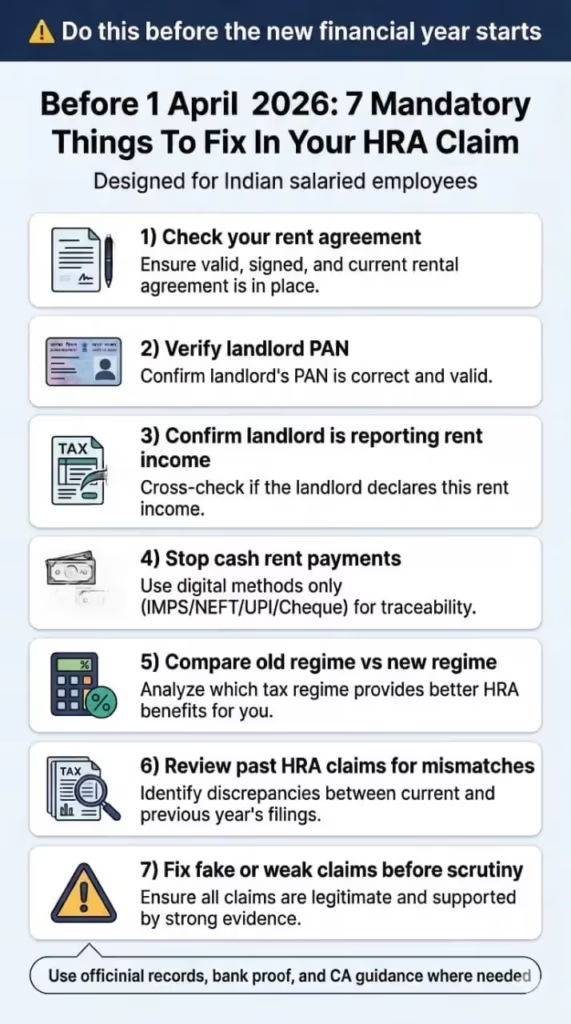

House rent allowance is one of the biggest tax-savers for working Indians, but Indian-Tax Rules 2026 have tightened the screws on how you claim it. If you are still relying on loose cash receipts and verbal agreements, your tax exemptions could be rejected or worse penalized.

Here’s your 7 point checklist to audit before claiming HRA as the new financial year begins.

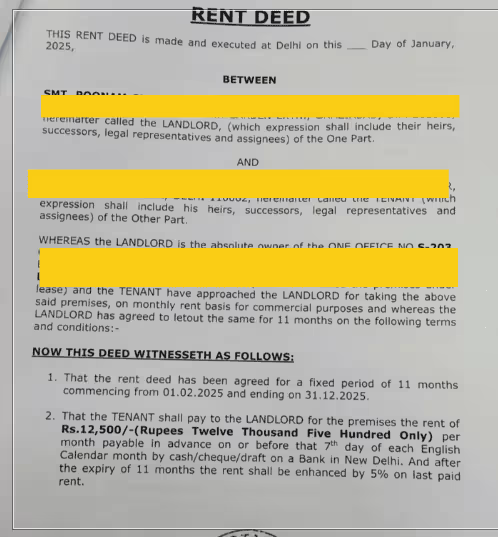

Audit before claiming HRA by scanning Your Rental Agreement (Add your City’s status)

The Rule: The way your HRA exemption is calculated depends entirely on where you live and rent you actually pay. The draft Rules brings massive news for Tech workers” Rule 279 now explicitly classifies Hyderabad, Pune, Ahmedabad, and Bengaluru in the same tier as Delhi and Mumbai.

The Action:

- Ensure you have a legally valid, signed and stamped agreement for the financial year as rent agreement serves as a foundational legal proof of your tenancy.

- Review your rent to ensure the address clearly falls within these city limits. If you live in these cities, you are now eligible for 50% of salary exemption limit (up from 40%)

- Ensure your agreement covers the entire financial year (April 1st to March 31st) and the rent amount perfectly matches what you plan to claim.

Ask your CA: "Does my current agreement meet the documentation standards to survive an automated tax-department flag?"The Queries to keep in mind:

“Is rent agreement mandatory now?”

Rent agreement establishes the legal arrangement between landlord and tenant which has been made mandatory under draft income tax rules, 2026.

“Are rent receipts enough?”

Rent receipts are proof of payment but no longer a bullet proof shield alone as the genuineness comes from the disclosing, whether obligation to pay exists or not. The Landlord- tenant relationship has to be known via House Rent Agreement and explicitly added under draft income tax rules, 2026.

“Can I claim HRA if the agreement is not registered?”

Draft rules do not explicitly state that rental agreements must be registered to claim HRA. But ensure that your rent agreement is properly executed on stamp paper, signed, and the amount strictly matches with bank transfers you made to your landlord.

“What if the agreement address and office records don’t match?”

This is a massive red flag. The draft Rules 279, HRA exemption limit is strictly based on location of your residential accommodation. Falling short of this primary compliance will make you ineligible to claim HRA and triggers scrutiny. So Ensure that address on your rent agreement perfectly matches with your current address you have declared to HR records

“Can I make an agreement now for the past months?”

Creating backdated paperwork to claim HRA is error prone and risky behavior and it can easily be exposed under ‘actual rent paid’ scrutiny of tax authorities. Therefore, it is recommended to have current agreement even in informal family arrangements.

Discover More Related Post

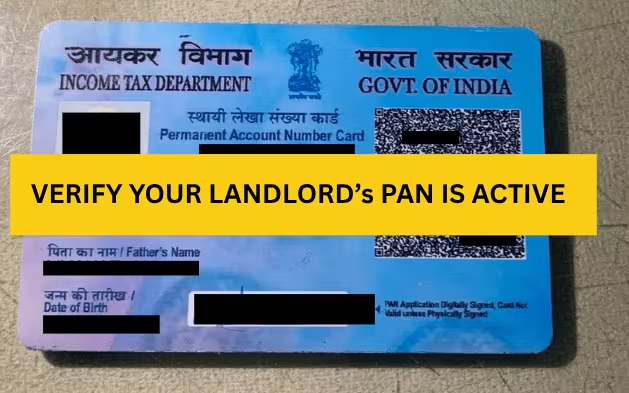

Verify Your Landlord’s PAN is Active (“The 1 Lakh Rule”)

The Rules: Under new Rule 205, you cannot simply hand over rent receipts to HR anymore; you must legally declare your evidence using Form No. 124. If your aggregate rent paid in a year exceeds Rs. 1,00,000 (Just Rs. 8,333/- month). You must furnish the name address and PAN of your landlord in this form.

The Action:

This is a critical compliance checkpoint.

- Check if you have your Landlord’s valid PAN.

- Form 124 also requires you to declare your relationship with the Landlord (e.g.: father, spouse, unrelated) Do not attempt to mask the rent to relatives as an arm-length transaction without proper documentation.

Ask your CA: "My rent is over ₹1 lakh, but my landlord is refusing to share his PAN. What exact alternative document or declaration can I submit to HR right now so my HRA claim isn't completely rejected under the Form 124 rules?""The Queries to keep in mind:

“My landlord refuses PAN — can I still claim HRA?”

In case, the landlord explicitly refuses to provide his PAN, then the possibility of qualifying for the HRA Exemption is negligible at the best. In case your landlord has no PAN, only in such cases you can provide the declaration along with payment proofs and rental agreements.

“Is Aadhaar mandatory or optional here?”

Aadhar is mainly for address verification While PAN is more primary as through it, the details of rent receipts can be auto-populated and cross-verified across two accounts ( landlord and tenant’s account) Under Draft Rules, 2026, the linking of Aadhar with PAN has become mandatory for all individuals, Its non-compliance will render PAN inoperative from 1st April 2026. Inoperative PANs attract higher penalties, inability to receive refunds and high value transactions.

“What if the landlord is a parent and does not file ITR?

You must still provide their PAN, if their total income (including your rental income)falls below the basic taxable limit, they don’t necessarily have to pay tax but your declaration will link the transaction to their PAN in the government’s database.

Confirm Your Landlord is Actually Reporting the Income

The Rule: By forcing you to file Form 124, the tax department is actively mapping your HRA exemption directly from your landlord’s return.

The Action:

– Have a transparent conversation with your landlord. Inform them that their PAN will be officially submitted in your Form 124 to the income tax department.

– If they are not actively declaring your rent as “Income from House Property” in their own tax returns, the system will easily catch the mismatch, which could trigger notices for both of you.

Ask your CA: "How can I legally verify if my landlord is actually declaring the rent I pay him in his own taxes? Is there a specific document I should ask him for before the financial year ends to ensure our records match?"The Queries to keep in mind:

“Can I still claim HRA if I pay rent to parents?”

Paying rent to parents or relatives has never been explicitly denied anywhere in draft tax rules 2026. However, claims must be supported by formal rental agreement showing the genuine tenancy arrangement or with whom ownership of the property actually lies must be addressed to tax authorities under draft income tax rules, 2026. It was specifically done to curb the fake HRA exemptions claimed by salaried employees for years.

“What should I write about my relationship with the landlord?

Draft income tax rules promote transparency, compliance & accountability so be truthful about the disclosure of the relationship with the landlord. So while disclosing you must accurately state the relationship as ‘parents’, ‘siblings’, ‘spouse’, or ‘unrelated’.

“Will paying rent to relatives cause scrutiny?”

Transactions involving the tenancy arrangement with relatives will make you come under the high scrutiny and vigilance of the Income Tax Department but that does not mean exemption claims will be substantively disqualified without merit. If the substantial disclosures have been furnished by both sides including rental agreements, verified payment methods proving the commercial substance, it will be perfectly permissible under those circumstances.

“Can I leave this field blank if the landlord is my father?”

Absolutely not, this is the mandatory field introduced under draft income tax rules 2026. Leaving this field as ‘Blank’ will make the whole HRA claim viewed under the greater precision of Tax Authorities. It is recommended to fill in the appropriate details of the actual relationship you have. Such Disclosures do not make the HRA claim disqualified without merit.

“Is rent to spouse valid for HRA?”

Paying rent to your spouse is not disqualified prima-facie under draft income tax rules, 2026. However, tax authorities would scrutinise the commercial substance of the transaction and genuine payment of rent till verification. Individuals would attract penalties only in case of misreporting or under reporting on income under section 270A under Income tax Act, 1961.

Stop Cash Payments Immediately

The Rule: The Rule 205 demands that you furnish solid “evidence of expenditure”. While cash used to work before, tax scrutiny relies heavily on verifiable financial trails. The draft rules legally recognize specific electronic modes of payment (like UPI, NEFT, RTGS, and IMPS) under Rule 48.

The Action:

- To make claims foolproof, immediately halt all cash payments for rent.

- Transition entirely to verifiable banking channels so that they match the exact date and amount on your rent agreement.

- This claim is an undeniable audit trial that proves rent was actually paid from your account, which is the best defense if your claim is ever scrutinized.

Ask your CA: "My rent agreement is for ₹30,000, but I transfer ₹25,000 via UPI and pay the remaining ₹5,000 in cash for maintenance. How exactly should I fill out Form 124 so this discrepancy doesn't trigger a 'mismatched payment trail' notice?"The Queries to keep in mind:

“Is cash rent valid for HRA?”

The draft income tax rules, 2026 highly stresses on ‘expenditure actually incurred’ for the payment of rent. While a small amount in cash as rent, will still be considered. However, if your rent amount exceeds Rs. 1 Lakh it must be through verified payment methods as cash payment leaves no verifiable financial footprints. Your transaction will be exposed under greater precision by the tax authorities.

“What proof is needed for actual rent paid?”

The Proof of digital financial trail of rent paid must be transparent. Under the new scrutiny parameters, the amount you declare on HRA form must perfectly match the “bank credits of the landlord”.

“Bank transfer missing for some months — can I still claim?”

You should only claim the HRA for the specific months where you have a no mismatched payment trail or otherwise,later, it will lead to scrutiny by tax authorities. In case you claim HRA where no rent was actually paid or having mismatched payment trails or you skipped paying rent for two months could trigger a mismatch notice.

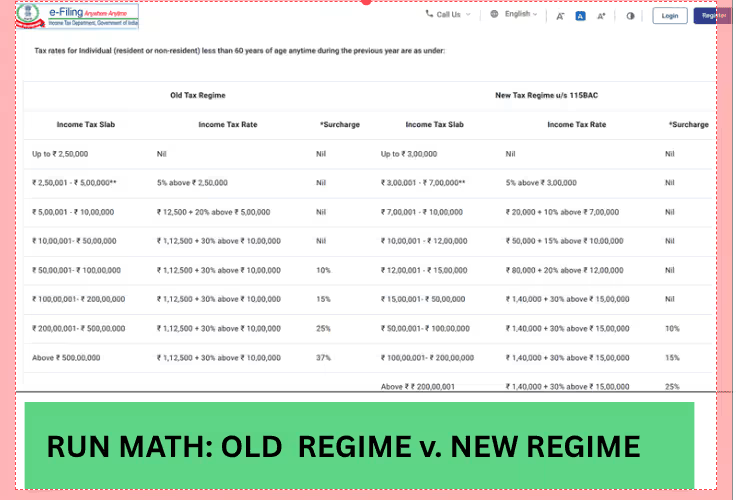

Run the Math: Old Regime vs. New Regime for HRA

The Rule: The choice of your tax regime dictates whether to claim HRA at all. Under Rule 136, individuals must officially exercise or withdraw their option for the new regime when filing their return of income.

The Action:

- You must decide which tax regime works best for you.

- Do the math now. If your rent is high (especially in the newly upgraded 50% cities like Bengaluru or Pune), the old regime with HRA deduction might save you significantly more money than the flat lower rates of the New Regime.

- Inform you HR of your choice in April so they deduct the correct monthly TDS.

Ask your CA: "I need to declare my tax regime to HR next week. Based on my current CTC and my rent agreement, can you calculate the exact 'break-even' rent amount where submitting proofs for the Old Regime gives me a higher in-hand salary?"The Queries to keep in mind:

“If I choose the New Regime with my HR in April, can I switch back to the Old Regime while filing my ITR if my rent increases?”

Yes you can. The choice you communicate to your employer in April dictates your monthly TDS, but it is not locked forever. Under Rule 136 of the draft rules, the official option to exercise or withdraw from the tax regime is made directly “in the return of income” furnished for that tax year.

“Since I don’t have my landlord’s PAN, my HR capped my HRA claim at ₹1 Lakh. Does this automatically mean the New Regime is cheaper for me?”

Not automatically but highly likely. Under Rule 205, if your aggregate rent paid during the year exceeds Rs. 1 Lakh, you are legally required to furnish the name, address, PAN and relationship with the landlord. If you cannot provide PAN, your exemption is effectively capped. Without the ability to claim HRA benefit, the old regime loses its primary tax-saving advantage.

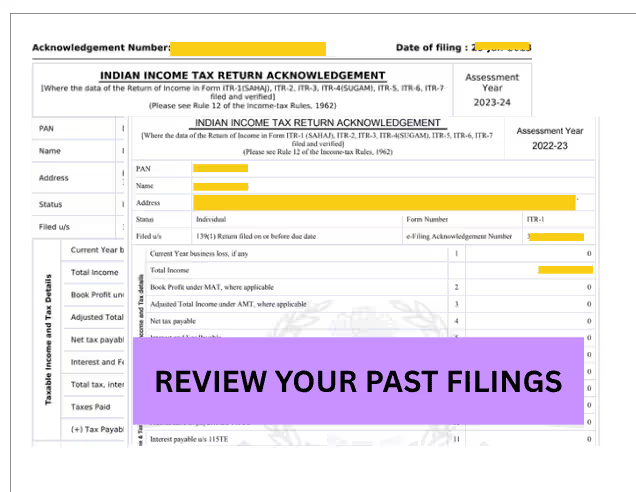

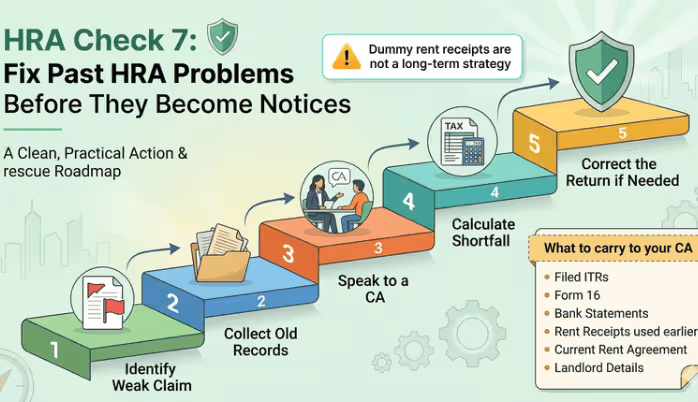

Audit Your Last 3 Years of Returns for Red Flags (Check for Mismatches)

The Rule: The tax department employs an “ automated examination tool” using artificial intelligence to scrutinize returns and mismatch. If your past HRA claims a valid PAN or didn’t match your bank statements, you are at the risk.

The Action:

- Download your previous tax returns (ITR) and Form 16s. Check if your HRA claim matches the rent actually transferred.

- If you spot a discrepancy, you have a window to fix it. Under Rule 165, you are allowed to furnish an updated Return (ITR-U) to correct omissions and misstatements from the past years.

Ask your CA: "I brought my last three years of ITRs and bank statements. Can you audit them against the new compliance rules and tell me if I am missing any mandatory disclosures that the automated system might flag?"The Queries to keep in mind:

“My landlord didn’t declare the rent I paid him last year. Will the new AI system flag my previous HRA claim as a mismatch?”

Yes, there is a severe risk of this. The draft rules 2026 officially deploys an ‘automated examination tool’ which is an algorithm that uses Artificial Intelligence (AI) and Machine Learning to conduct standard examination of returns. By forcing you to link your landlord’s PAN to your HRA claim under rule 205, the system can automatically cross reference your claimed rent deduction against the landlord’s declared income. One sided transaction is a prime trigger for a mismatch notice.

“How far back can the new ‘Faceless Assessment’ system dig into my past tax filings?”

The draft income tax requires you to keep your books of accounts and other documents for a period of seven years from the end of the relevant tax year. Furthermore, the rules cover “faceless reassessment” procedures under section 279 through an automated allocation system. If AI tools detect historical mismatches your past filings within those statutory limits are fully exposed to automated scrutiny.

“I claimed HRA using cash receipts for the last two years. Will this be automatically rejected if my case is picked up for scrutiny now?”

While paying in cash isn’t explicitly illegal, the compliance guidelines flag ‘relying on self made receipts’ and ‘mismatched payments trails’ are highly error-prone behaviour. The law bases the HRA benefit strictly on the ‘expenditure actually incurred’ by the assessee. Without a verifiable digital bank to prove the rent was actually paid, your claim is incredibly weak and highly susceptible to rejection during scrutiny assessment.

Clean Up Past “Adjustments” Before the Department Does by Consulting a “CA”

The Rule: With the introduction of mandatory forms like form 124 and automated tracking, fake or dummy rent receipts are ticking time bombs. Filing an incorrect return can lead to your return being treated as a “defective return” under Rule 166 or invite heavy penalties during an automated faceless assessment.

The Action:

- If you have previously submitted fake or dummy rent receipts to save tax, do not panic but do act. Consult a Chartered Accountant Immediately to understand your liability, potential penalties, and how to rectify your filing strategy moving forward.

- They can help you file an updated return under Rule 165 to voluntarily pay deficit tax before the tax department’s automated system flags you for a penalty.

Ask your CA: "I claimed ₹1.5 Lakhs HRA last year without a real rent agreement. What is the exact process, timeline, and financial cost (deficit tax + fee) to file an Updated Return (ITR-U) right now to reverse this before I get caught?"The Queries to keep in mind:

“I used ‘dummy’ rent receipts last year to save tax. How do I legally fix this before I get a tax notice?”

You can legally fix past misstatements by filing an Updated Return (ITR-U). Rule 165 prescribes the specific form (ITR-U) and procedures for furnishing an updated return of income. This allows you to voluntarily reverse the fake deduction, recalculate your actual tax liability, and pay the deficit tax before the department’s automated tools flag the mismatch.

“If I file an ‘Updated Return’ (ITR-U) to reverse my fake HRA claim, will it automatically trigger an audit?”

No. The updated return mechanism under Rule 165 is designed precisely to encourage voluntary compliance. It is a government- sanctioned window to cover omissions or misstatements without inherently triggering a combative penalty.

“What happens if I just leave my old ‘fake’ HRA claims as they are, but start following the strict 2026 rules from this year onwards?”

You are leaving a time ticking bomb. The deployment of ‘automated examination tools’ means past returns can be systematically scanned for mismatches (such as missing landlord PAN or rent amount in form that is not matching bank credits of the landlord). Leaving old fake claims exposes you to sudden faceless reassessment.

“What exact documents should I take to my CA to ensure my past ‘adjustments’ are cleaned up safely?”

You need to provide a complete picture so the CA can calculate the exact deficit. Bring your filed ITRs, your Form 16s, your bank statements (which will reveal the lack of actual rent transfers), and the “dummy” receipts you used. For the current year, if you wish to claim legitimate HRA, ensure you take your valid Form No. 124 details—which must include your formal rent agreement, bank transfer proofs, and your landlord’s PAN if rent exceeds ₹1,00,000

Conclusion

The landscape of HRA claims in 2026 has shifted from a trust-based system to a digitally-mapped ecosystem. With the introduction of Rule 205 and Form 124, your tax exemption is now an auditable legal claim rather than a simple payroll deduction. Relying on loose cash receipts or verbal agreements is no longer a viable strategy; the tax department’s AI-driven “automated examination tool” is specifically designed to flag mismatches between your claims and your landlord’s disclosures.

To protect your hard-earned income, you must transition to a verified financial trail. If your past filings contain “adjustments,” the window for Updated Returns (ITR-U) under Rule 165 offers a legal path to compliance before the system triggers a faceless assessment. In this new era of taxation, a proactive audit today is the only way to prevent a costly penalty tomorrow.

Leave a Reply