Faceless Hearing Does Not Resolve the Issue, then, Final Assessment Order will be passed by the Assessing Officer (AO). So, either you can pay the tax demand or file for Appeal before commissioner or joint commissioner.

Quick Answer

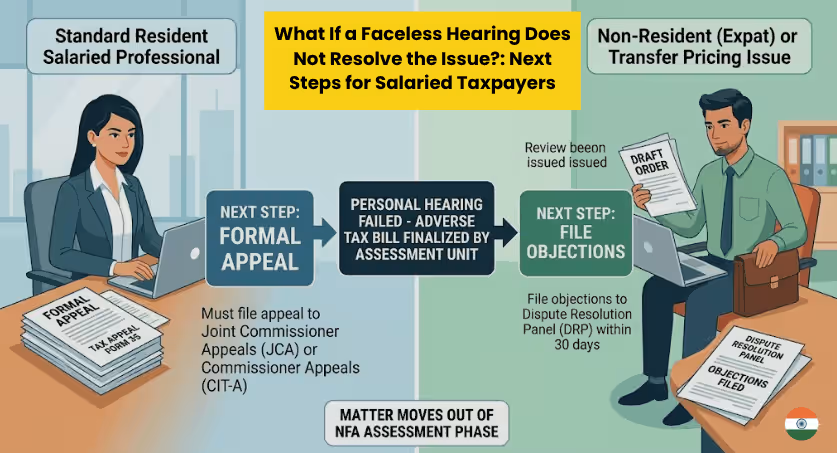

If personal hearing does not resolve the issue and “Assessment Unit” finalizes an adverse tax bill against you, then, the matter moves out of the NFAC Assessment Phase your next step depends upon your status, for example:

- If you are Standard Resident Salaried Professional: you must file a formal appeal against final assessment order to the joint commissioner appeals or commissioner appeals.

- If you are Non-Resident (Expat) or those with Transfer Pricing Issues: you will be issued a “Draft Order” you have 30 days to escalate the matter by filing your objections directly with the elite Dispute Resolution Panel.

Introduction

You attended the virtual personal hearing, presented your evidence, but the Faceless Assessment Unit still ruled against you. What happens next?

Once the hearing concludes unfavorably, the Assessment Unit will pass a final assessment order, and the National Faceless Assessment Centre (NFAC) will serve you a Notice of Demand under Section 289 under Income Tax Act, 2025 specifying the exact amount of extra tax, interest, and penalties you owe.

Check Out: When Can You Request a Personal Hearing After an Income-Tax Notice 2026?What If, you are dissatisfied with the final Assessment Order ?

At this point, the assessment stage is completely over. You now have to make a choice: pay the demand, or escalate the dispute. Here is the exact roadmap for salaried taxpayers.

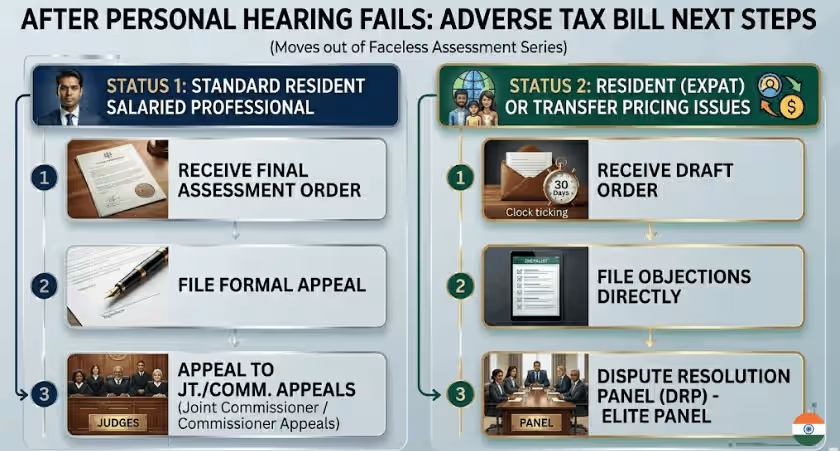

Stage 1: The Appeals Route (For Standard Residents)

If you are a standard Indian resident and you completely disagree with the tax demand, your immediate next step is to file a formal statutory appeal.

- Where to file: You must file an appeal before the Joint Commissioner (Appeals) or the Commissioner (Appeals) under Section 356 or 357.

- The Deadline: You only have 30 days from the date the notice of demand is served on you to file this appeal.

- The Cost: Filing an appeal is not free. You must pay a fee based on your total income (ranging from ₹250 to ₹1,000). Furthermore, you must generally pay the tax due on the income you did admit to in your original return before the appeal can be admitted.

- Why you need a CA here: An appeal is a quasi-judicial process. You must file a formal “Form of Appeal” accompanied by “Grounds of Appeal”. You cannot introduce new evidence at this stage unless you can legally prove the Assessing Officer refused to admit it earlier.

Stage 2: The Dispute Resolution Panel (For Non-Residents & Expats)

If your residential status for the tax year was “Non-Resident” (for instance, you just moved back to India or are an expat), the rules completely change.

- The Draft Order: The Assessing Officer cannot send you a final tax demand immediately. By law, they must first serve you a “Draft Order” under Section 275 of Income Tax Act, 2025.

- Your 30-Day Window: Upon receiving this Draft Order, you have 30 days to file objections directly with an elite body called the Dispute Resolution Panel (DRP).

- The Benefit: The DRP is a collegium of three senior Commissioners. While your objections are pending before the DRP, the Assessing Officer is blocked from finalizing your tax bill or forcing you to pay.

Discover More Related Post

The Alternative Route: Paying the Tax and Claiming Immunity

If the tax demand is relatively small, or you realize you actually did make a mistake in your return, fighting a years-long appeal might cost more in CA fees than the tax itself. However, accepting the tax bill usually triggers severe penalties for under-reporting income.

The Strategy: Under Section 440 of the 2025 Act, you can apply for Immunity from Imposition of Penalty. If you pay the demanded tax and interest within the notice period, and you legally promise not to file an appeal, you can apply to the Assessing Officer for complete immunity from the dreaded misreporting penalties and prosecution. The Assessing Officer must grant this immunity if the conditions are met (provided the concealment wasn’t categorized as willful misreporting).

What the reader should do next:

The moment you receive a final assessment order and a Demand Notice, the 30-day countdown begins. Download the order, your original “Hash Result” submission receipts, and your Annual Information Statement, and immediately hand them to a Tax Professional to draft your Grounds of Appeal.

Check Out: Can You Handle a 142(1) Notice Yourself or Should You Consult a CA? A Complete Decision Guide for Salaried Professional

Leave a Reply