If you are a salaried person and have received an Income Tax Notice Under Section 268(1) under Income Tax Act, 2025 or formally 142(1) under Income Tax Act, 1961 ? What It Means, Why You Got It, and What to Do Next…

Introduction

Receiving an income-tax notice can feel stressful, but this page is here to help you understand the notice before you react. For salaried professionals, this type of notice usually means the department wants a pending return, supporting documents, or an explanation for a mismatch or transaction. In this guide, you will understand what the notice is asking, what to check first, how to reply carefully, and when it makes sense to seek professional help.

Quick answer: what is this notice (formally called 142(1) usually means?

This Notice is simply an “Inquiry Before Assessment”, meaning the Tax Department is giving you a deliberate opportunity to explain the discrepancy and file the missing paperwork before they make any adverse tax calculation against you:

- To file your tax return in case you have missed the deadline

- Specific accounts, documents, or foreign bank statements, in case needed

- Written explanations (for example: “explain the source of the rupees 10 lakh deposit on 4th August 2025”)

“This is serious, but manageable if you read the notice carefully and respond on time.”

Check Out: Income-Tax Rules 2026: Key Payroll Changes for Salaried Employees in FY 2026–27The 2 most common reasons you may receive it

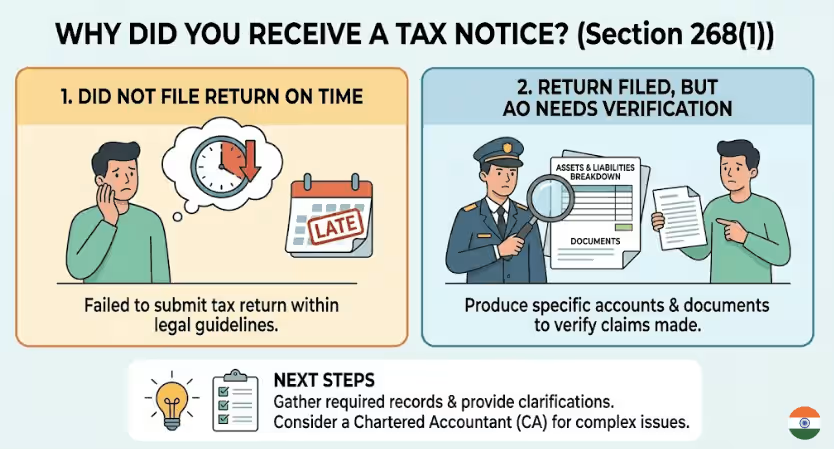

It is important to understand why a Notice under section 268(1) is served to the salaried professional and what the purpose behind this Notice is.

This Notice is received if you fall into one of these two categories:

- A salaried professional did not file the tax return within the legal guidelines, or

- You did file your return, but the Assessing Officer (AO) needs you to produce specific accounts, documents, and written statements, like a breakdown of your assets and liabilities, to verify the claims you have made.

For example, a person who has filed his return but forgot that he made high-value transactions this year, like huge mutual fund investments or purchased a luxury car or a property, and such transactions are reflecting in his AIS but not showing in his return. Now this has triggered a major mismatch which has been detected by algorithms, and therefore he has received an auto-generated tax Notice from the Income Tax Department.

There can be another example, like a person who is earning or who has earned this year from freelance income in which the client has deducted the TDS, and he might have not disclosed or forgot to disclose the transaction, but the algorithm or the system has detected the transaction, and therefore he has received the Notice for the explanation or the clarification or to show the relevant documents to the Assessing Officer (AO).

How the notice is usually delivered?

Ever since the Income Tax Department has automated its operations, which has been reflected in the Income Tax Act, 2025, Notices are no longer served by the local tax officer. They are served centrally by the National Faceless Assessment Centre (NFAC). Now salaried professionals will not merely receive a physical letter, and as per the Income Tax Act, 2025, in most cases the Notice is considered “served” when it is:

- uploaded to your registered e-filing account on the designated tax portal.

- sent to your registered email address.

- uploaded to the Income Tax mobile app.

Every Notice is followed by a “Real-Time Alert” such as SMS or an app notification, to inform you that a document has been delivered.

“Do not rely on email alone; also check the portal.”

Step-by-step: what to do after receiving the Notice under section 142(1)

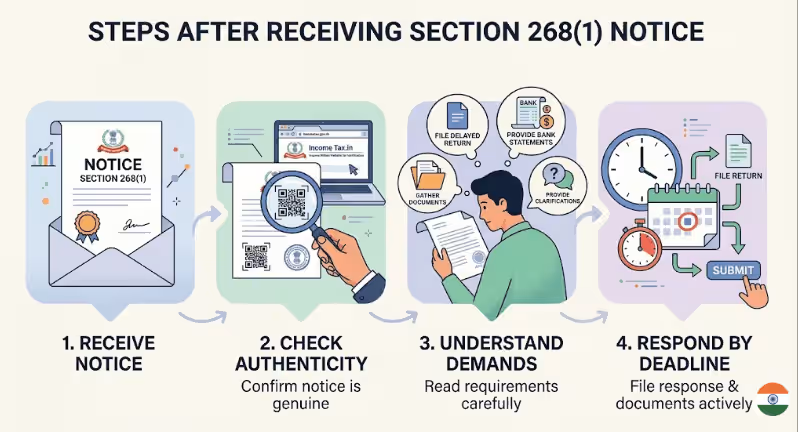

- CHECK THE AUTHENTICITY

If you have already received the Notice under section 268(1), confirm by yourself the authenticity of the Notice received. Check the User Manual to authenticate whether the Notice is issued by the Income Tax Department.

(Read More: https://www.incometax.gov.in/iec/foportal/help/how-to-authenticate-Notice) - READ THE NOTICE CAREFULLY.

See what is demanded: Are they asking you to file the delayed return? Or are they asking for specific bank statements, documents, a complete summary of assets and liabilities, or clarifications? What are the directions issued by them? - NOTE THE RESPONSE DEADLINE

Strictly adheres to the deadline for a 268(1) Notice response. Because there is no universal statutory last date to file a response under the Income Tax Act, 2025. The exact date and time by which you must reply will be specified directly inside the Notice sent to you.

(Know more about the consequences for non-filing or delayed filing of Notice.)

- FILE THE RETURN, IF NOT FILED

File the return, in case you have not filed the return, or - GATHER THE RELEVANT DOCUMENTS

Gather the exact documents and bank statements requested, or provide them with the necessary clarifications or explanations if needed. Then submit your response actively. - SAVE THE PROOF OF SUBMISSIONS

Download the acknowledgement after submission.

Check Out: consequences for non-filing or delayed filing of Notice under section 268(1) or 142(1)

How to reply without making common mistakes

Now Notices are auto-generated, and the responses are read by an algorithm, or you can say a faceless officer who doesn’t know you. So, a few things you should keep in mind while submitting or replying to the Notice you have received. This will help you avoid further Notices in the future.

Practical tips for replying to a section 268(1) notice:

- Never data dump: For example, if the Notice asks about a 5 lakh deposit, only explain that specific deposit by providing the bank statement showing the transfer and the brief explanation (like, “gift from father”). Do not upload your entire year’s financial history, as over-sharing gives the algorithm more data to scrutinize. So, answer precisely what is asked, nothing more.

- Use the “Genuineness” Defense: The tax law is built on intent. If you have made an honest mistake, you can defend yourself. For example, section 470 of the Income Tax Act, 2025 explicitly states that no penalty shall be imposed if the assessee proves that there was a “reasonable cause” for the failure.

For example: politely point out the clerical error you have made and attach the actual proof there, or if your HR department gave you an incorrect Form 130 and you relied on it, show that document as proof of your honesty and protect yourself from misreporting penalties. - Use the “hash result” Acknowledgement: Every response you submit on the NFAC portal, an electronic acknowledgement (containing a “hash-result”) is generated upon successful submission (a unique cryptographic digital footprint). Always save this. If the portal glitches and the AO claims that you didn’t reply, this “hash-result” is your absolute legal proof of compliance.

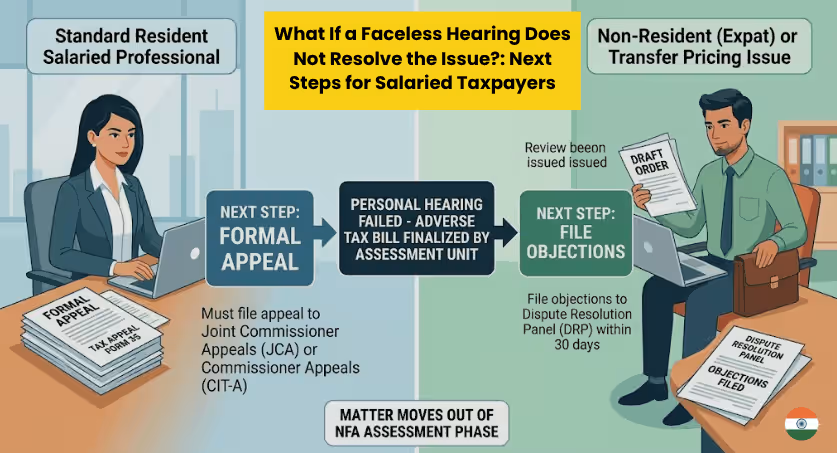

Pro Tip: Always save the PDF of this hash result. It is your absolute, indisputable legal proof that you submitted your reply on time.- Request for personal hearing, in certain circumstances: This right is not at all absolute but strictly conditional. So if you have received a Notice under section 268(1) via NFAC, and you have submitted your response including the required documents, statements, or explanations.

However, if the Assessing Unit is not satisfied, has rejected your claims, increased your tax or penalized you, and in parallel, has prepared a “Show Cause Notice” (SCN) stating variations prejudicial to your interest, now this is the exact moment when you are allowed to request a personal hearing.

(Learn more about the list of scenarios where a salaried employee can request a personal hearing.)

Discover More Related Articles

Can you handle it yourself or should you consult a CA?

In reality, from filing of return to receiving an Income Tax Notice, in a majority of cases, you don’t always need a CA, but you must know when your case crosses from simple to complex transactions. Because identifying such complex transactions would give the salaried professional a basic idea of when the cost would be incurred to them.

For example: If you simply forgot to file your return and your only income is salary and a few savings accounts, and in such an instance you have received a Notice. If such a Notice asks you to file your pending return or demands a basic document (like an investment receipt to claim for an 80C deduction or bank account statement or any written application), then you can upload it yourself without the involvement of experts.

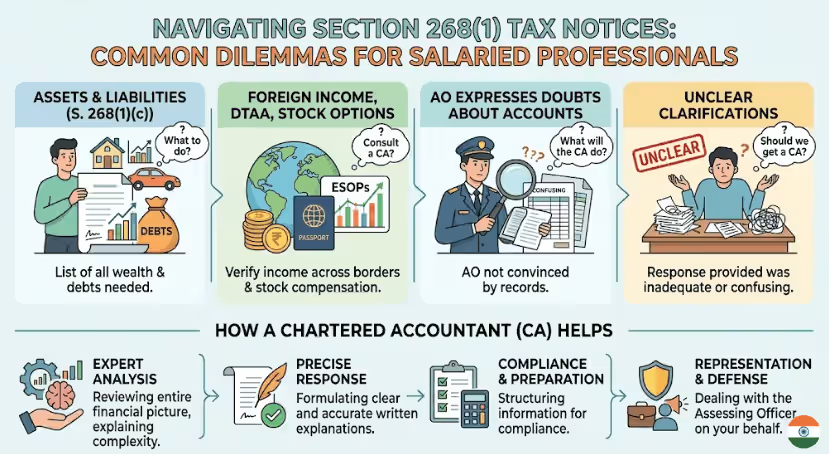

There are mainly the following instances that salaried professionals would find in the Notices received by them under section 268(1) that create a dilemma: what to do next? Should we consult a CA? What exactly would a CA do in these circumstances?

- Asking for Statement of Assets and Liabilities (Section 268(1)(c))

- Requiring inquiry into foreign income, DTAA, or stock options

- When the AO expresses “doubts about the correctness of the accounts”

- When required clarifications are not provided clearly

(Learn more about these consultation realities in detail if you are vigilant to know what you’re paying for.)

Check Out: Can You Handle a 142(1) Notice Yourself or Should You Consult a CA? A Complete Decision Guide for Salaried Professional

How to reduce the chance of future notice under section 142(1)?

When it comes to tax compliance, complacency acts as a silent catalyst for legal friction. Many salaried professionals fail to treat their tax filing with the same precision they apply to professional deliverables.

Here are the ways to stay away from dreaded Income Tax Notices.

- Reconcile the AIS (Form No. 168): The Annual Information Statement tracks your financial footprints. For example: if you sold a car, traded crypto, or bought a house, it will all reflect in this document. Never file your return without ensuring it matches your AIS perfectly.

If your return doesn’t match the AIS, the automated system will instantly trigger a Notice to you. - Do not solely rely on employer salary certificates: Your employer only deducts the tax on the salary they pay you. They do not account for your freelance income, capital gain, or foreign interest. Consolidating your global income is your legal responsibility.

- Update your portal email: Notices are legally served to the email on your e-filing portal or your Aadhaar database. If your portal has an old corporate email from the job you left, you will miss the Notice, fail to reply to such Notice, and would attract consequences with the best judgment order.

- Consolidate your Form 130s (Salary Certificate) if you switched jobs: If you changed employers during the year, you must declare your previous salary to your new employer using Form No. 122. Both employers will issue certificates of tax deducted at source in Form No. 130 (the new equivalent of Form 16).

Failing to aggregate the income of all Form 130s in your final return will instantly trigger an intimation under section 270(1) of the Income Tax Act, 2025 for an incorrect claim, as the CPC algorithms will automatically detect the omitted salary and demand the tax shortfall. - Quote PAN carefully for high-value lifestyle expenses: The tax department tracks your spending to ensure it aligns with your declared salary. You are legally required to quote your PAN for specific high-value transactions.

If the algorithms detect these high-value PAN footprints but your filed salary is disproportionately low, it will trigger an Inquiry Notice under Section 268(1) of the Income Tax Act, 2025. - Track mandatory filing triggers (even if your salary is below taxable limits): You must file a return by the standard deadline (usually July 31st for salaried individuals). Even if your total income is below the taxable limit, the rules strictly mandate that you must file a return if you trigger certain expenditure thresholds during the year.

Such as: If you hit any threshold and fail to file, the Faceless Assessment Centre will automatically issue a 268(1) Notice compelling you to furnish a return.

Check Out: PAN Quoting Rules 2026: Compliance Guide for Salaried EmployeesKey takeaways

Salaried professionals must not be scared of the Notice under section 268(1); it is an opportunity for them to explain the discrepancies that have been reflected in their return and traced by the algorithm.

You might have received the Notice for either of these reasons: either you have not filed your return, or the Assessing Officer needs certain documents, statements, or explanation for the transaction that is reflecting in your AIS but not reflecting in your return. It is not a situation of panic when you have received the Notice.

Instead, you just have to be under constant vigilance as soon as you receive the Notice, like carefully reading the Notice, ensuring the deadline to reply to this Notice, and seeing what specifically has been conveyed or directed by the Assessing Officer in the Notice. There are certain circumstances where the involvement of the CA is recommended.

However, in the majority of cases, you can deal with the reply to the Notice under section 268(1) by yourself just by knowing how to reply smartly and take the necessary precautions to keep avoiding such Notices in the future.

Leave a Reply