Quick Answer

As a salaried professional, you cannot immediately request a personal video hearing the moment you receive a standard income-tax notice. Under the Income-tax Act 2025, the right to a personal hearing is only triggered after you have submitted your written documents, and the tax department officially proposes to increase your tax liability or reject your deductions by serving you a formal “Show Cause Notice”

What do you mean by Personal Hearing?

Under Income Tax Act, 2025 the right to a personal hearing can be simply stated as an “oral opportunity of being heard”, which is legally guaranteed to salaried individuals (and all assesses) across several specific sections.

What is the process of “Faceless Hearing” work?

Under the faceless tax system a personal hearing does not mean visiting the income tax office physically. No personal appearance is allowed, instead, hearing is conducted exclusively through video conferencing or video telephone via the National Faceless Assessment Centre (NFAC) portal.

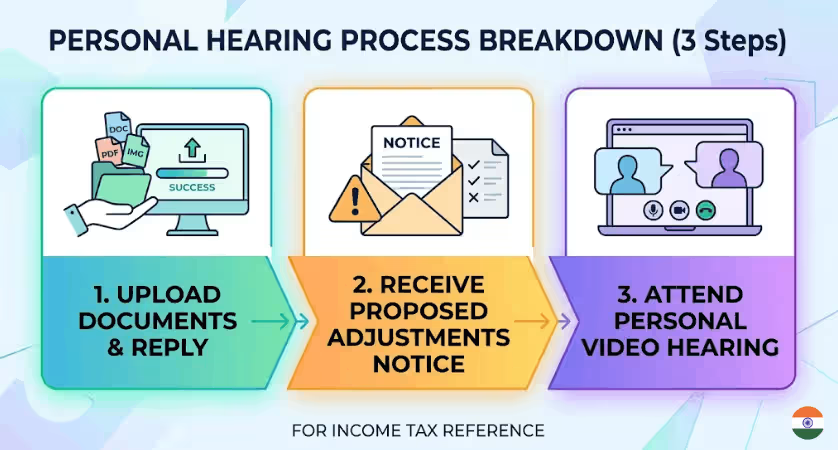

Here, is how Personal Hearing under Faceless Assessment works (Section 273):

- The Inquiry stage: The right to personal hearing is subjected, at the request of salaried professionals. So when you have received a 268(1) notice via NFAC and thereafter you prepare a reply by uploading the PDFs, bank statements and explanations required; however, there is no video call here at this stage.

- The Show Cause stage: If the “Assessment Unit” is not satisfied with your reply and decides to reject your DTAA claim or added your foreign stock options to your taxable income then, and then will issue a “Show Cause Notice” proposing certain variations, which are prejudicial to your interest.

- Requesting the hearing: When such Show Cause Notice is served on you demanding your explanation why your claims should not be rejected. Then, you or your authorized representative may request a personal hearing to make oral submissions.

If salaried professionals have requested, the Income-Tax Authority must allow the hearing, which will be conducted through video conferencing via the NFAC portal.

While there is no lifetime limit, it is generally a one-time event per show Cause Notice. If the Tax Department later issues a separate notice, (for example proposing heavy tax penalties) after the assessment is done, you have a fresh right to be heard before the penalties are finalized.

Certain Cases where salaried employee can request a Personal Hearing

Here are a few cases, in which personal Hearing becomes highly relevant:

During Assessment and Scrutiny Proceedings

- Special Audit Inquiries under Section 268: If the Assessing Officer directs a special audit or inventory valuation, you must be given an opportunity of being heard regarding any material gathered from that audit before it is utilized in your final assessment.

- Best Judgment Assessment: As per section 271, If you fail to file your return or ignore tax notices, the Assessing Officer cannot pass a unilateral “Best Judgment” assessment without first serving a notice to show cause and giving you an opportunity of being heard.

Check Out: Received an Income-Tax Notice under section 268(1) (formally called 142(1))? A First-Response Guide for Salaried ProfessionalsDuring GAAR (General Anti- Avoidance Proceedings) under section 274

If the Tax Department suspects you of participating in a tax dodging arrangement, before invoking GAAR proceedings against you, both, Principal Commissioner and the elite Approving Panel must provide you an opportunity of being heard before issuing any direction that is prejudicial to your interests.

During Penalty and Immunity Proceedings

- Imposition of Penalties under section 471 and 476: No order imposing, enhancing, or reducing a penalty (such as the penalty for misreporting income) can be made unless you have been given a reasonable opportunity of being heard.

- Immunity from Penalty: As per section 440, If you accept a tax demand, pay it, and apply for immunity from penalty and prosecution, the Assessing Officer cannot reject your application without giving you an opportunity of being heard.

During Appeals and Dispute Resolution

- Section 359 relates to Appeals to Joint/Commissioner Appeals: When you file a formal appeal against a tax demand, you have the right to be heard at the hearing of the appeal, either in person or through an authorized representative (like a CA).

- Dispute Resolution Panel – DRP under section 275: If your case goes to the DRP, the panel cannot issue any directions that are prejudicial to your interest without giving you an opportunity of being heard.

During Rectifications, Transfers, and Administrative Actions

- Clubbing of Income under section 99 : If the income of your spouse or minor child was already taxed in their hands (or the other parent’s hands) in a previous year, the Assessing Officer cannot suddenly club that income into your tax return without giving you an opportunity of being heard.

- Transfer of Case under 243 or Change of officer under 244: If the Tax Department wishes to transfer or replace your case from one Assessing Officer to another in mid (unless the transfer is within the same city/locality), you must be given a reasonable opportunity of being heard/reheard.

- Rectification of Mistakes under section 287: If an Income-Tax Authority wants to amend a past order to fix an apparent mistake, and that amendment increases your tax liability or reduces your refund, they must give you a notice of their intention and a reasonable opportunity of being heard.

- Section 434 (Refund Rejections): If you apply for a refund claiming that tax was wrongfully deducted at source and should be returned, the Assessing Officer cannot reject your application without giving you an opportunity of being heard.

What to prepare before requesting a Personal hearing ?

Because your time on the video call will be limited, you must be fully prepared for personal hearing. You should have:

- Your Annual Information Statement (AIS) (Form No. 168): To cross-reference the exact high-value transactions the officer is questioning.

- Hash Result Acknowledgements: Every time you previously uploaded a document to the NFAC, the system generated a “hash result”. Have these ready to prove you submitted your evidence on time.

- Exact Statutory Proofs: If defending an exemption, have your Form 130 (salary certificate) and the actual bills (like medical or rent receipts) ready to share on your screen.

Can you attend personal hearing yourself or through a CA?

You have the legal right to attend the video hearing personally. However, the law also explicitly allows you to attend through an “authorised representative”. For salaried professionals, this authorized representative is typically a Chartered Accountant (CA) who holds a valid certificate of practice.

During such a conference, you or your authorised representative (like CA) will directly address the Income Tax Authority of the relevant Assessment unit and make oral submissions by presenting your screen to show the evidence (like Bank Statements or Rent Agreements) and explain exactly why the proposed tax addition or rejected deduction in their “Show Cause Notice” is incorrect.

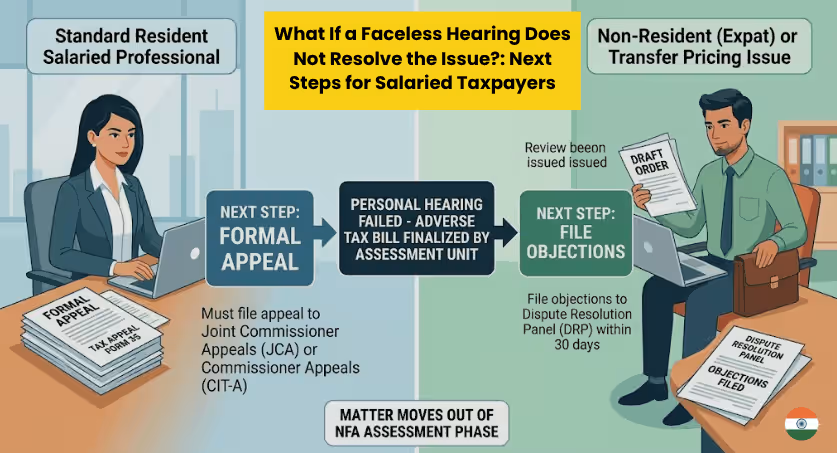

Check Out: Can You Attend a Personal Hearing Yourself or should you Consult a CA? (For More detail)What if the issue is still not resolved?

If the video hearing or Personal Hearing does not convince the Assessment Unit, they will proceed to pass a final assessment order and the NFAC will serve you a demand notice specifying the extra tax you must pay.

Once this final order is passed, the faceless assessment stage closes, and you must move to the formal appeals process to fight the tax demand

Check Out: What If a Personal Hearing Does Not Resolve the Issue? Next Steps for Salaried Taxpayers (For More Detail)Does every income-tax notice come with a Personal hearing?

No. The vast majority of initial notices do not come with an option for a hearing. If you receive an Intimation under Section 270(1) for a math error, or a Notice of Inquiry under Section 268(1) asking for your rent agreement or bank statements, the entire process is strictly document-based. You are legally required to upload your response electronically to the National Faceless Assessment Centre (NFAC). At this preliminary stage, there is no officer to talk to, and no video link will be provided.

How the Personal hearing process works

The era of visiting a physical income-tax office is over. The National Faceless Assessment Centre (NFAC) completely eliminates the physical interface between you and the tax authority. If you request a Personal Hearing in response to a Show Cause Notice, the income-tax authority must allow it.

The hearing will be conducted exclusively through video conferencing or video telephony (using software provided by the tax department). The officer on the screen could be located anywhere in India, and they will only discuss the specific tax variations proposed in your notice.

Leave a Reply